Employment Practices Liability Insurance, known as EPLI, is defined as a policy that covers businesses against employee claims including wrongful termination, discrimination, harassment, and retaliation. Understanding why HR needs employment practices liability protection is not optional for any organization with employees. Federal laws like Title VII of the Civil Rights Act, the Americans with Disabilities Act, and the Age Discrimination in Employment Act create legal exposure for every employer, regardless of size. Small businesses face the greatest risk, yet most operate without EPLI, leaving them one lawsuit away from a financial crisis. Quickhrtx works with Texas businesses daily and sees this gap firsthand.

Why HR needs employment practices liability coverage now

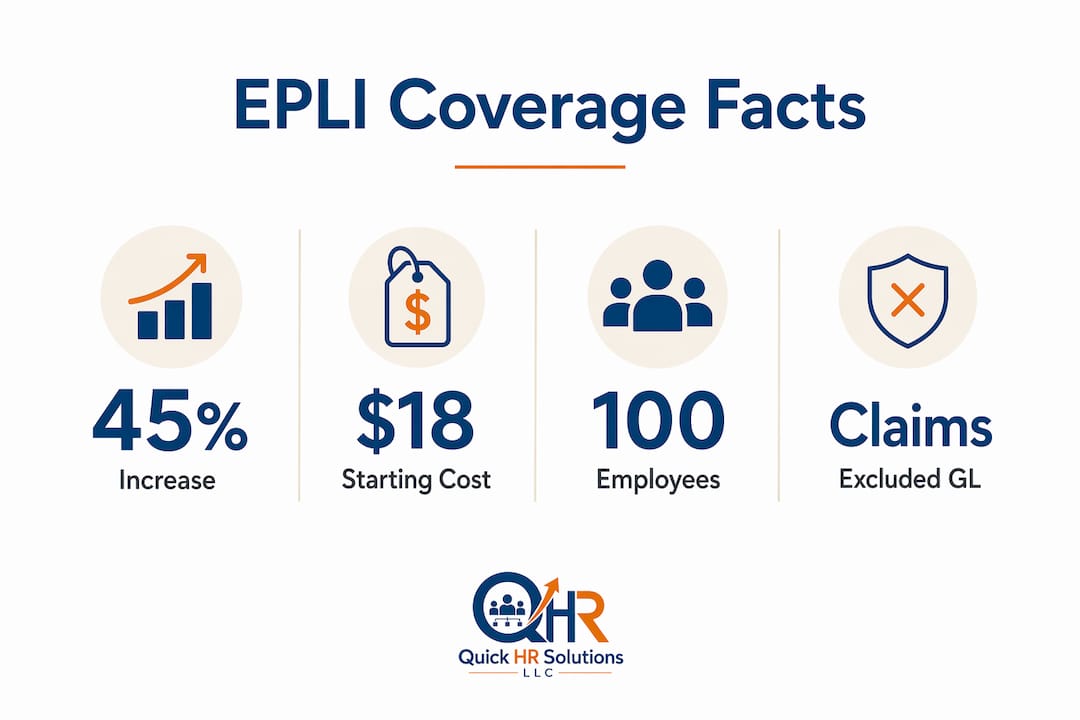

Employment claims are not just a large-company problem. Employers with fewer than 100 employees face significant litigation risks, yet most lack any EPLI protection. A single wrongful termination claim can cost tens of thousands of dollars to defend, even when the employer wins. That financial reality makes the importance of employment practices liability impossible to ignore.

The legal environment has grown more complex since 2020. Discrimination claims have increased, and three emerging forces are accelerating the trend. AI-driven hiring tools introduce algorithmic bias claims. Wage transparency laws in states like Colorado and New York create new grounds for pay equity disputes. Return-to-office mandates generate accommodation and retaliation complaints. Each of these trends adds a new category of exposure that did not exist a decade ago.

Social inflation compounds the problem. Higher settlements and defense costs are now standard in employment litigation, driven by plaintiff-friendly juries and aggressive legal strategies. This means even a claim that settles quickly carries a significant price tag.

Common claim types EPLI covers

- Wrongful termination: Claims that a firing violated public policy, an implied contract, or anti-discrimination statutes

- Discrimination: Allegations based on race, gender, age, disability, religion, or national origin under Title VII, the ADA, or the ADEA

- Sexual harassment: Both quid pro quo and hostile work environment claims

- Retaliation: Claims filed after an employee reports a violation and then faces adverse employment action

- Wage and hour disputes: Allegations of unpaid overtime or misclassification under the Fair Labor Standards Act

- Failure to promote: Claims that advancement decisions were made on discriminatory grounds

Does general liability insurance cover employment claims?

General liability insurance specifically excludes employment-related claims. This is the most dangerous misconception HR professionals and business owners carry. A GL policy covers bodily injury, property damage, and advertising injury. It does not cover a harassment allegation or a wrongful termination lawsuit. The gap is absolute, not partial.

The financial consequences of that gap are severe. Even meritless claims cost thousands to defend out-of-pocket when no EPLI policy exists. Attorney fees alone in an employment case routinely reach $50,000 before a case reaches trial. For a small business in Texas, that figure can wipe out an entire year of operating profit.

EPLI also operates differently from most other business insurance. EPLI is a claims-made policy, meaning a claim must be reported while the policy is active. If a business cancels its EPLI policy and a former employee files a claim six months later, that claim receives no coverage. Tail coverage, also called an extended reporting period endorsement, closes that gap. Businesses that are changing carriers or closing operations must purchase tail coverage to avoid retroactive exposure.

Pro Tip: Review your EPLI policy renewal date every year alongside your employee handbook review. Letting either lapse at the same time doubles your risk exposure.

The cost of EPLI is far lower than most business owners expect. Some providers offer endorsements starting at about $18 per employee per year. That figure makes EPLI one of the most cost-effective risk transfers available to any employer. Defense costs and attorney fees, which EPLI covers, are consistently the largest expenses in employment claims regardless of whether the employer is ultimately found liable.

How strong HR practices and EPLI work together

EPLI is not a substitute for good HR. It is the financial safety net that catches you when good HR is not enough. The two work best together, and pairing EPLI with specialized HR support including state-specific policy updates and manager training significantly improves defense outcomes.

Here is how HR professionals can build that integrated approach:

- Maintain a current employee handbook. Policies on harassment, discipline, and termination must reflect current federal and Texas state law. An outdated handbook can be used against you in litigation.

- Train managers consistently. Most employment claims originate from a manager's decision, not an HR policy. Annual training on documentation, accommodation requests, and termination procedures reduces that risk directly.

- Document every significant employment decision. HR professionals must document all benefits counseling conversations and employment decisions to avoid "he-said/she-said" liability scenarios. A written record of the reason for a termination is your first line of defense.

- Treat benefits administration as a liability area. Benefits administration poses a unique counseling risk where informal HR advice can create binding employee expectations. An HR team member who tells an employee they are "definitely covered" for a procedure creates a potential claim if that turns out to be wrong.

- Audit your HR compliance posture annually. Texas employers face both federal requirements and state-specific rules. An annual HR compliance review catches gaps before they become claims.

Pro Tip: When an employee raises a complaint, write a summary of the conversation within 24 hours and store it in a secure HR file. That document becomes critical evidence if the situation escalates.

The SHRM Body of Competency and Knowledge identifies risk management as a core HR competency. HR professionals who hold SHRM-CP or SHRM-SCP credentials are trained to view documentation, policy consistency, and legal compliance as daily responsibilities, not reactive measures. That mindset is exactly what EPLI insurers reward with better coverage terms and lower premiums over time.

What to consider when evaluating EPLI for your organization

Selecting the right EPLI policy requires more than comparing premiums. The wrong coverage limit or a missing endorsement can leave you exposed at the worst possible moment.

- Coverage limits: Most small businesses need at least $1,000,000 per claim. Companies with rapid growth, high turnover, or recent HR complaints should consider higher limits.

- Deductibles: EPLI deductibles typically range from $1,000 to $25,000. A higher deductible lowers your premium but increases your out-of-pocket cost when a claim hits.

- Third-party coverage: Standard EPLI covers claims from employees. Third-party endorsements extend coverage to claims from customers, vendors, or contractors who allege discrimination or harassment.

- Tail coverage: Always ask about the cost of tail coverage before signing with any carrier. This is especially critical for businesses in growth mode that may switch carriers frequently.

- Industry-specific risk: Restaurants, healthcare organizations, and staffing firms carry higher employment claim frequencies. Insurers price EPLI accordingly, and your broker should know your industry's claim history.

- Existing policy audit: Many business owners assume their Business Owner's Policy or workers' compensation coverage includes employment claims. Neither does. No general liability policy covers employment claims, and assuming otherwise is a costly mistake.

Work with a broker who specializes in employment practices coverage, not a generalist who adds EPLI as an afterthought. Ask specifically whether the policy includes access to HR hotlines, sample policies, or compliance resources. Many EPLI carriers bundle these services at no additional cost, and they directly reduce your claim frequency. For a deeper look at the full risk picture, the HR risk management strategies that complement EPLI are worth reviewing before you meet with a broker.

Key Takeaways

EPLI is the only insurance product that covers employment-related claims, and no business with employees can afford to operate without it.

| Point | Details |

|---|---|

| GL insurance does not cover employment claims | General liability policies exclude wrongful termination, harassment, and discrimination claims entirely. |

| Small businesses carry the highest risk | Employers with fewer than 100 employees face significant litigation exposure but rarely carry EPLI. |

| Claims-made structure requires tail coverage | EPLI only covers claims reported during the active policy period; tail coverage prevents retroactive gaps. |

| HR practices reduce claim frequency | Consistent documentation, manager training, and updated policies lower both claim rates and defense costs. |

| Benefits counseling is a hidden liability | Informal HR advice on benefits can create binding expectations and trigger claims under EPLI. |

The cost you are not calculating

Most HR leaders I work with focus on the dollar amount of a potential settlement. That is the wrong number to watch. The real cost of an employment claim is the six to eighteen months of management distraction that follows a lawsuit filing.

The indirect costs of employment claims, including administrative disruption and management time lost, are consistently underestimated. When a claim lands, your HR team stops doing HR. They pull records, meet with attorneys, respond to discovery requests, and sit in depositions. Your managers spend hours reconstructing decisions they made two years ago. Your leadership team loses focus on the business. None of that shows up in a settlement figure, but all of it is real.

Even organizations with perfect employee handbooks need EPLI because perfection does not prevent claims. It only improves your defense. A disgruntled former employee can file a complaint with the EEOC at no cost to themselves. Your defense starts the moment that complaint arrives, regardless of its merit.

My honest recommendation is this: buy EPLI before you think you need it, pair it with strong HR documentation practices, and treat the combination as your baseline risk posture. The businesses I see struggle most are the ones that waited until after a claim to ask whether they were covered.

— John

How Quickhrtx supports your EPLI risk management

HR liability insurance benefits are maximized when your internal HR practices are tight. Quickhrtx provides fractional HR consulting for small and mid-sized Texas businesses, covering the exact areas that drive EPLI claims: policy development, manager training, documentation protocols, and compliance updates.

Whether you need a full fractional HR consulting engagement or targeted support on a specific risk area, Quickhrtx delivers SHRM-certified expertise without the overhead of a full-time HR department. Texas employers face a layered compliance environment, and having an experienced HR partner on your side reduces both claim frequency and the cost of defending the claims that do arise. Book a free consultation at quickhrtx.com to review your current exposure.

FAQ

What does EPLI actually cover?

EPLI covers employment-related claims including wrongful termination, discrimination, sexual harassment, retaliation, and failure to promote. It pays both defense costs and settlements up to the policy limit.

Does my business owner's policy include EPLI?

Standard Business Owner's Policies do not include EPLI coverage. Employment claims require a separate EPLI policy or a specific endorsement added to an existing policy.

How does EPLI help small businesses in Texas?

EPLI protects small Texas businesses from the cost of defending employment claims, which can reach tens of thousands of dollars even when the employer is not at fault. It also provides access to HR resources that reduce claim frequency.

What is tail coverage in an EPLI policy?

Tail coverage extends the reporting period after an EPLI policy expires or is canceled. Without it, claims filed after the policy ends receive no coverage, even if the underlying incident occurred while the policy was active.

How does HR documentation reduce EPLI claims?

Thorough documentation of employment decisions, disciplinary actions, and benefits counseling conversations creates a factual record that supports your defense and discourages frivolous claims from moving forward.